Most people probably already know the terms Converged infrastructures (CI) and HyperConverged Infrastructures (HCI) that are both become quite common in the IT world, with several products and solutions that aim to be fit in those classifications. With the addition of new terms, like composable infrastructures.

But HCI has become a hot topic with several vendors that aim to be a leader in this area, or with several “magic quadrants” that try to define who is in.

And most people say that HCI market will just eat all (or most) of the primary storage market.

But how really big is this market and which are the main players in the HCI world?

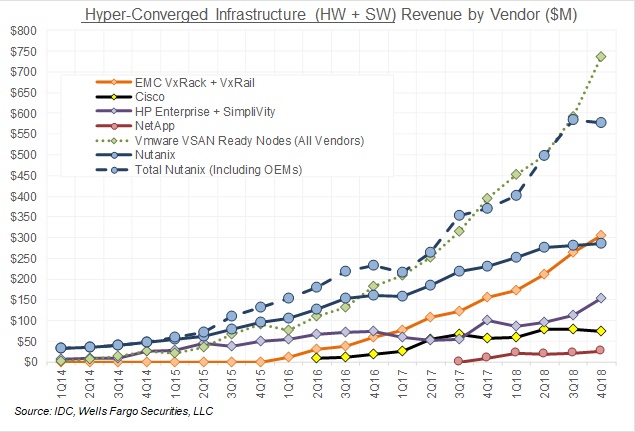

There is an interesting article (VMware accelerates HCI growth, Nutanix stumbles, Cisco declines) with an analysis or hyperconverged infrastructure supplier revenue by Wells Fargo analyst Aaron Rakers that give some interesting data for until the end of Q4 2018:

Why is interesting: because it’s clear that most of the HCI market is around VMware vSAN and Nutanix AOS technologies. And they are really close with a similar trend for both of them (if we consider the aggregation of all vendors for vSAN and the aggreagation for all the alliance for Nutanix).

HPE Simplivity seems far from the top and with the recent announce will be probably slow down (and make Nutanix grow instead).

NetApp Solidfire and the “HCI” branded products seems really far away and not yet mature for this market or the market has not yet understand how there can be HCI by de-coupling storage and compute node (see also: What’s really define an HCI solution? ).

Funny that Microsoft with is S2D and the AzureStack solution is not there at all, but I guess that this analisys just cover the hardware based market, where instead the software part could be also interesting (considering the related server market).

Other small vendors, like StarWind or Scale Computing also seems excluded, but I’m not so sure that the SMB market could be so minimal and not relevant at all.

Anyway is really clear which are the main competitor.

And what about the future of the storage world? Will the HCI solutions replace other (external) storage solutions?

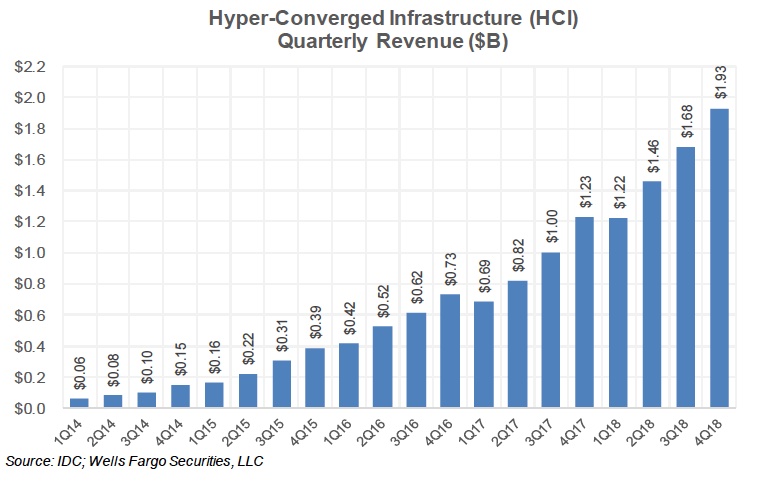

If we look at the grow seems that there is an exponential grow:

Is the 2019 the year of HCI?

We can look at some analisys of the overal storage market like those from IDC:

- Worldwide Enterprise Storage Market Grew 34.4% during the First Quarter of 2018, According to IDC

- Worldwide Enterprise Storage Systems Market Revenue Grew 7.4% During the Fourth Quarter of 2018, According to IDC

According to the International Data Corporation (IDC) Worldwide Quarterly Enterprise Storage Systems Tracker, the total worldwide enterprise storage systems factory revenue grew 34.4% year over year during the first quarter of 2018 (1Q18) to $13.0 billion. and has increased 7.4% year over year to $14.5 billion during the fourth quarter of 2018.

So really not the same numbers… HCI remain far from the big market, that means a possible grow in the future maintening interesting trends for several years… but still far to replace other solutions.

And HCI is not for all the use cases, or at least, customer are able (and free) to choose the proper solutions. And there are several signs that demostrate this (for example let’s consider how the VMware Cloud Foundation has changed to include also external storage).

Like the VDI, at this time, HCI is not a killer application that totally changed the storage world. But has change a part of it and has become a reality and a new option.

Maybe the large adoption of NVMe over Fabric will bring again more changes in the future.

Related Posts

Andrea Mauro

Virtualization, Cloud and Storage Architect. Tech Field delegate. VMUG IT Co-Founder and board member. VMware VMTN Moderator and vExpert 2010-24. Dell TechCenter Rockstar 2014-15. Microsoft MVP 2014-16. Veeam Vanguard 2015-23. Nutanix NTC 2014-20. Several certifications including: VCDX-DCV, VCP-DCV/DT/Cloud, VCAP-DCA/DCD/CIA/CID/DTA/DTD, MCSA, MCSE, MCITP, CCA, NPP.